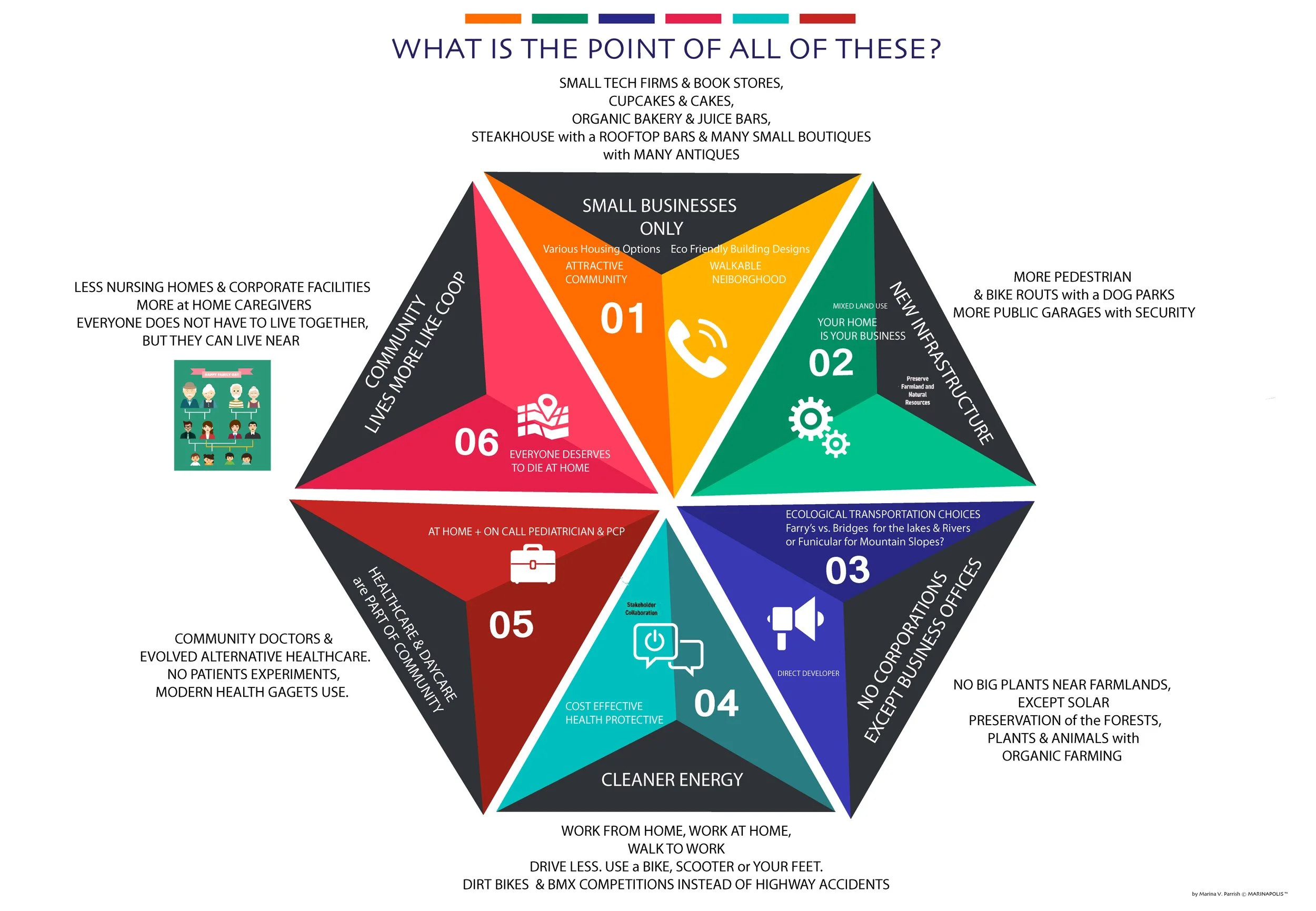

Preventing a banking monopoly in a small development community

Preventing a banking monopoly in a small development community using internal financing while maintaining control over infrastructure and sales prices requires a hybrid model that blends community-based, cooperative financing with rigorous, legally enforced land-use agreements. Key strategies involve establishing a community land trust, leveraging local community development financial institutions (CDFIs), and creating a resident-controlled entity to manage infrastructure.

Key strategies involve establishing a community land trust, leveraging local community development financial institutions (CDFIs), and creating a resident-controlled entity to manage infrastructure.

Here is a framework to achieve these goals:

1. Structure Internal Financing to Prevent Monopoly

Instead of relying on a single large developer or bank, create a competitive, decentralized internal financing structure.

Establish a Community Land Trust (CLT): The community or a nonprofit entity holds ownership of the land, while residents own their homes. This structure allows the community to set resale prices, ensuring permanent affordability.

Utilize Community Development Financial Institutions (CDFIs): Instead of using a traditional bank, partner with a CDFI or create a local credit union. CDFIs allow communities to maintain control over underwriting and relationship-based lending, keeping capital "local".

Create a Loan Pool/Consortium: Multiple small, local investors or residents can pool capital to fund infrastructure or housing projects, distributing risk and ensuring no single entity controls the financing.

Internal Financing Mechanisms: Implement a system where homebuyers pay a percentage of their mortgage interest into a local community fund, rather than to an external bank.

2. Maintain Control Over Local Infrastructure

To prevent a private entity from holding infrastructure hostage, control must be transferred to a collective body.

Form a Community Improvement District (CID) or HOA: A resident-controlled HOA or Municipal Utility District (MUD) can own and maintain roads, utilities, and public spaces.

Infrastructure Financing through Assessments: The MUD can issue municipal bonds to pay for infrastructure up-front, allowing residents to pay it back over time, rather than relying on a developer to fund it and take control. This way municipality has more control over the general infrastructure.

Community Benefits Agreements (CBAs): Use legally binding contracts between developers and community members to ensure the developer provides agreed-upon infrastructure, parks, or amenities.

3. Maintain Control Over Sales Prices AND MAINTAINING QUALITY OF LIFESTYLE

To keep homes affordable and prevent speculative monopolies, you must restrict the resale value.

Resale-Restricted Covenants: Place legal covenants on properties that limit the maximum resale price, ensuring homes remain affordable for future buyers, a common technique in CLTs.

Right of First Refusal (ROFR): The community entity (e.g., trust or HOA) retains the "right of first refusal" to buy back any property before it is listed on the open market, allowing it to maintain the price level.

Land Use and Zoning Constraints: Work with local municipal officials to enforce strict density, building types, and development standards, ensuring the development remains aligned with community needs rather than profit-maximization.